3DS

Initiate a 3-D Secure 2.x session for a card payment. This is the first step in any card flow that requires strong customer authentication. The endpoint returns a reference_id that must be attached to the subsequent Create Payment request.

When to Use

- Before creating a card payment when your acquiring region (e.g. EEA / UK) or issuer mandates 3DS 2.x

- Before any card transaction where you want the liability shift that 3DS provides

- Whenever your risk model requests strong customer authentication for a high-value transaction

- When your frontend needs a device fingerprint collection snippet for a compliant authentication flow

You do not need to call this endpoint when:

- The payment method is a wallet (

BINANCE_PAY,ALIPAY_PLUS_PAY) — those have their own authentication - You are using a server-to-server token that has already been 3DS-authenticated upstream

Endpoint

POST https://api.sandbox.build.app/api/v1/acq/3ds/setup

Integration Flow

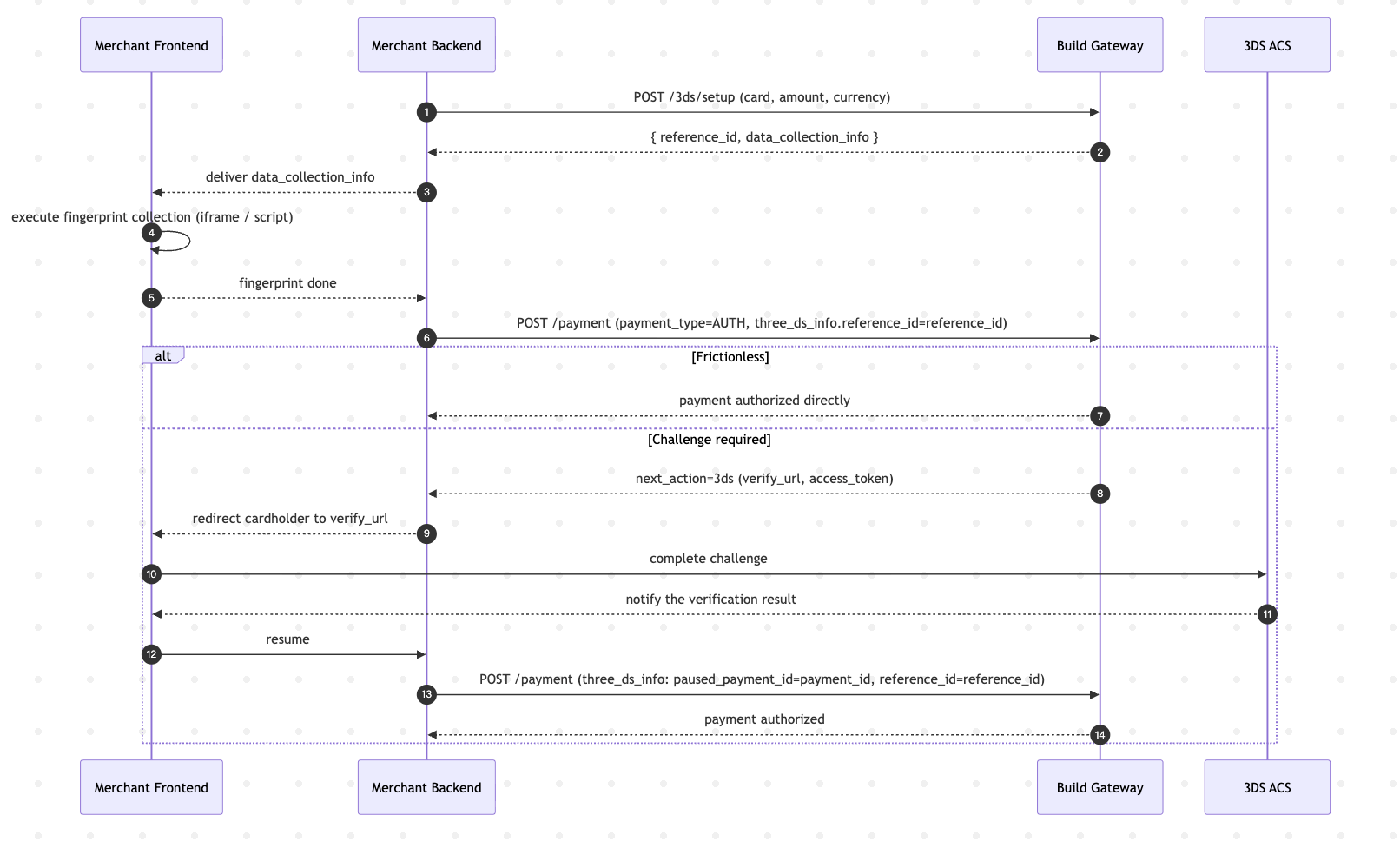

Numbered steps

- Your backend calls

POST /3ds/setupwith the card and amount. - Build returns a

reference_id(used to correlate the 3DS session) and adata_collection_infoblob. - Your frontend executes the device fingerprint collection using

data_collection_info. - Your backend calls

POST /paymentwithpayment_type=AUTH / DEBITand thereference_idinthree_ds_info. - If the payment responds with

next_action.type=3DS, redirect the cardholder toverify_urlto complete the challenge. - After receiving the 3DS authentication completion notification, resume the payment by calling

POST /paymentagain with thereference_idandpayment_id.

Best Practices

- Always pass

merchant_request_id. It is your idempotency key; retries with the same value return the first response within the 24-hour window. - Collect browser data accurately. Frictionless authentication depends heavily on complete

device_info. Missing fields (screen size, language, IP) lower your frictionless rate. - Pass full billing details (address + email). Issuers often downgrade to challenge if AVS fields are sparse.

- Do not cache

reference_id. It is bound to a single cardholder session. - Time-box the flow. If the cardholder has not completed Step 2 (device fingerprint) within ~10 seconds, you can proceed with a payment call.

FAQ

Q: Is 3DS mandatory for all card payments? A: No. It depends on your acquiring region, issuer requirements, and your risk policy. Build does not enforce 3DS by default — you decide when to call /3ds/setup.

Q: What happens if I skip /3ds/setup and call /payment directly? A: The payment may succeed (for non-3DS regions) or it may be declined with REQUIRES_ACTION. In the latter case, restart with /3ds/setup.

Q: Can I reuse a reference_id for multiple payments? A: No. Each reference_id is tied to one cardholder session and one intended payment amount.

Q: Frictionless vs Challenge — how do I know which path the cardholder will take? A: You don't know ahead of time. Always implement the challenge redirect logic (next_action.type=3DS). If the response comes back without next_action, the payment was authorized frictionlessly.

Q: The cardholder completes the challenge but my payment is still pending. What should I do? A: After receiving the 3DS authentication completion notification, resume the payment by calling POST /payment again with the reference_id and payment_id.

Next Steps

- Create Payment — attach the

reference_idinthree_ds_info