Refund Payment

Refund a captured or successful payment, either fully or partially. Funds are returned to the original payment instrument.

When to Use

- The customer requested a refund after receiving (or not receiving) the goods or service

- Fraud or chargeback prevention — proactive refund before the cardholder disputes

- Duplicate charge reversal

Do not use this endpoint when:

- The payment is still authorized but not captured → use Cancel Payment (faster, no fees)

- The payment itself failed (

payment_status=FAILED) — there is nothing to refund

Endpoint

POST https://api.sandbox.build.app/api/v1/acq/payment/{payment_id}/refund

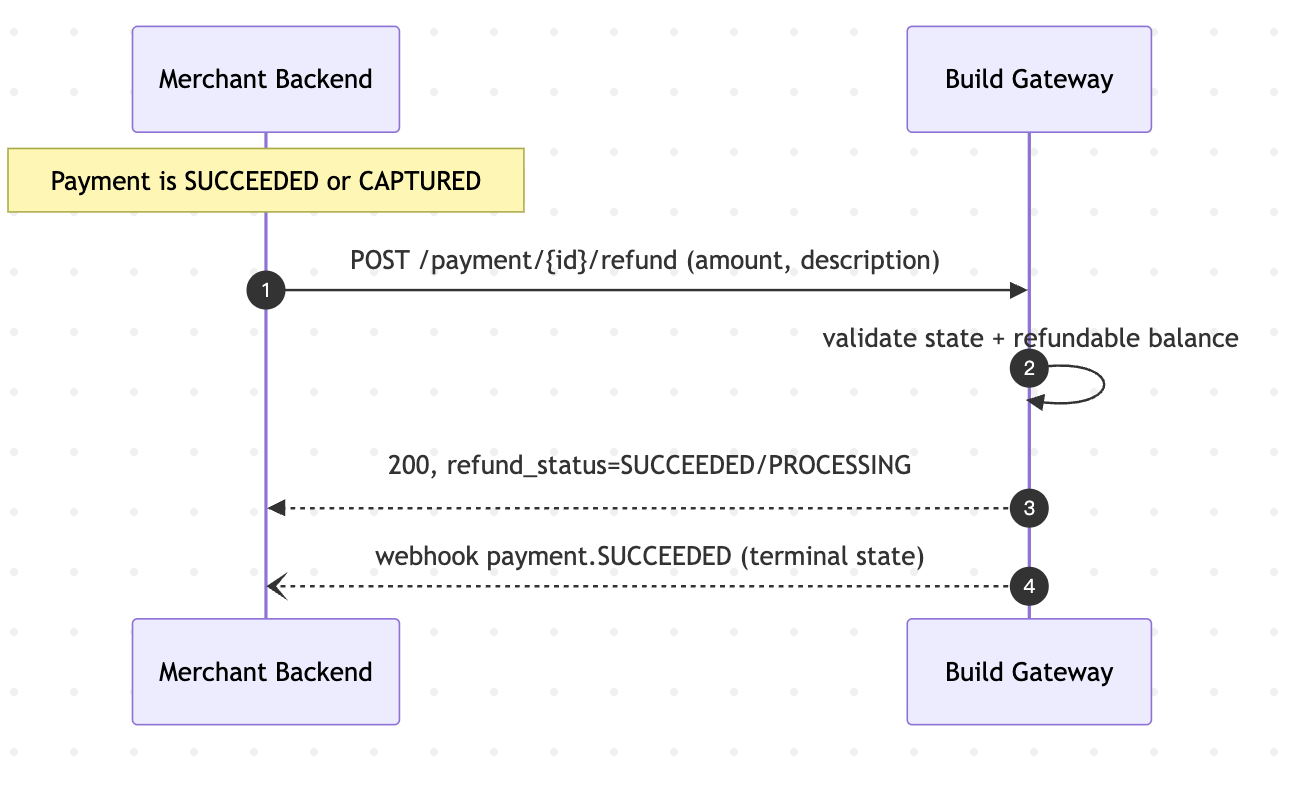

Integration Flow

Typical timeline to funds availability

Typical timeline to funds availability

| Payment method | Typical refund time |

|---|---|

CARD (credit / debit) | 1–5 business days to appear on the cardholder statement |

APPLE_PAY / GOOGLE_PAY | Same as underlying card |

BINANCE_PAY | Minutes to hours (on-chain confirmation) |

ALIPAY_PLUS_PAY | Same as underlying wallet (often same-day) |

The refund API response is typically near-instant (PROCESSING or SUCCEEDED). The time listed above is how long the cardholder waits to see the money back.

State Transitions

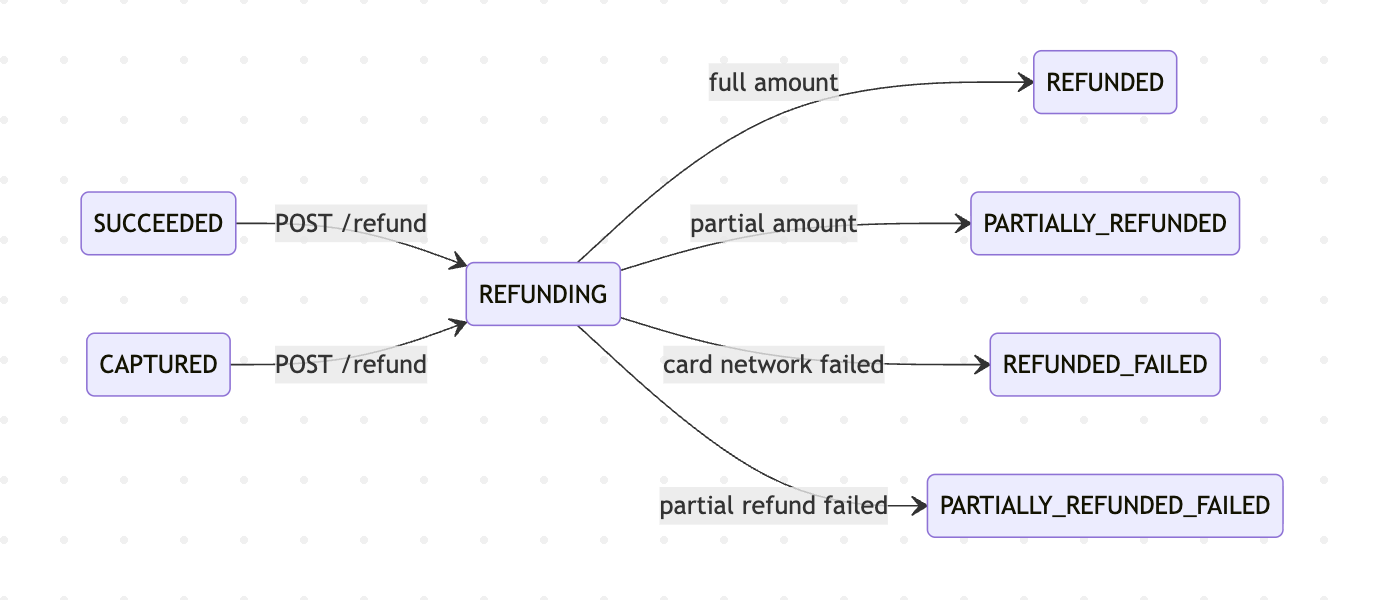

After a successful refund, the parent Payment transitions:

- Full amount refunded →

payment_status = REFUNDED - Partial refund →

payment_status = PARTIALLY_REFUNDED

Best Practices

- Always pass

merchant_request_id. Idempotency is critical to avoid double-refunds. Retries with the same value return the first response within the 24-hour window. - Query the payment first. Before refunding, verify the payment status and remaining refundable balance. Do not assume.

- Prefer Cancel over Refund when possible. If the payment is not still

CAPTURED, a cancel is instant and does not generate a pair of statement entries for the cardholder. - Set

descriptionresponsibly. For card networks, the description may surface to the cardholder's bank statement. - Reconcile via webhooks.

REFUNDwebhook is fired on terminal success. For synchronous card refunds the webhook fires within seconds. - Plan for failure modes. A refund can fail at the instrument level (closed bank account, expired card). Your operations flow should have a fallback (store credit, manual transfer).

- Track

refund_id, not justpayment_id. When you need to reconcile with settlement reports, therefund_idis the atomic unit.

FAQ

Q: Can I refund more than the original charge? A: No. Refunds cannot exceed the original payment amount (minus any prior refunded amount).

Q: Can I cancel a refund? A: No. Once a refund is submitted, it cannot be recalled through the API. If the refund is still PROCESSING, contact support immediately — there may be a narrow window before the funds leave your settlement account.

Q: My refund returned SUCCEEDED but the cardholder hasn't seen the money. What now? A: Card refunds take 1–5 business days to appear on statements — this is the issuer's pipeline. Wait 7 business days before escalating, and share the refund_id with support when you do.

Q: Do I get back the Payment processing fees when I refund? A: Fee return policy depends on your contract.

Q: Why is my refund still in PROCESSING after an hour? A: For card refunds, this is unusual — contact support. For crypto / on-chain refunds, network congestion can delay confirmation; wait for the webhook.

Q: The original payment method is no longer valid (card expired). Can the refund still succeed? A: In most cases, yes — card networks route refunds to the cardholder even on expired cards. In rare cases you will fail, contact the cardholder for an alternative channel.

Q: How do I refund a payment that is more than 180 days old? A: You cannot refund via the API. Contact support for manual reconciliation.

Q: Can I refund a specific line item of a multi-item order? A: Yes — use a partial refund with the matching amount.

Next Steps

- Cancel Payment — faster alternative for non-captured payments

- Create Payment — how to charge a customer in the first place

- Capture Payment — capture an authorization before refunding